Part 11: Cost Allocation Strategy

Main Idea

- Cost allocation is the discipline of assigning cloud spend to the right business owners, teams, products, or workloads.

- Good allocation makes cloud spending explainable, accountable, and actionable.

- It is one of the core foundations that allows the inform phase to produce useful answers instead of vague totals.

Why Allocation Matters

- Allocation makes it clear who is spending what.

- It enables teams to forecast their own growth, manage against budgets, and respond to anomalies with context.

- It also creates the visibility needed for showback, chargeback, and eventually unit economics.

Allocation Connects Cost to Business Value

- Cost allocation is the link between technical resource usage and business ownership.

- Once costs are mapped correctly, teams can connect spend to products, business units, and business outcomes.

- This is what makes value-based cloud decisions possible.

Why Allocation Is Hard

- Allocation is not just about setting up accounts and tags once.

- It is a moving target because organizations reorganize, shared costs appear, and untagged or untaggable resources are common.

- Different stakeholders also need different reporting views, so allocation must support multiple perspectives at once.

Different Personas Need Different Views

- Finance teams want spending tied to cost centers, products, and reporting structures.

- Engineers want service-level and usage-level detail that helps them understand operational impact.

- Leaders want rolled-up views across teams and portfolios.

- A good allocation strategy supports all of these needs without losing consistency.

Unit Economics Depends on Allocation

- Teams cannot meaningfully discuss unit economics unless spend is attributed correctly.

- Allocation makes it possible to tie business metrics to cloud costs.

- This helps organizations focus on efficiency and value, not just raw spend reduction.

Amortization Matters

- Upfront payments for reservations, commitments, or discounts can distort cost reporting if not handled properly.

- Cloud spend should often be reported on an accrual basis rather than a simple cash basis.

- This matters when commitments or discounts have upfront payments whose value is realized over time.

- Amortization spreads those upfront costs into the periods where the benefit is actually used.

Example:

- Here is a simplified example of amortization and the resulting savings.

- On-demand rate: $0.10 per hour.

- Reservation cost: $200 up front, plus $0.05 per hour when used.

- Amortized hourly rate:

- Effective savings: $0.027 per hour, or about 27%.

Why Amortization Improves Reporting

- Without amortization, spending appears artificially low when teams use prepaid commitments.

- That creates confusion when accounting later applies the real cost treatment.

- With amortization, reporting, forecasting, anomalies, and chargeback all align around a more accurate picture of actual spend.

Simplified Amortization Example

- On-demand usage might cost more per hour than a reserved or committed rate.

- The upfront cost of the reservation should be spread across the usage period.

- The result is an amortized hourly rate that reflects the true effective cost and the actual savings gained.

Use Amortized Data Everywhere

- Mature FinOps reporting includes amortized prepayments, adjusted rates, and shared costs in the data teams see.

- Forecasting, anomaly detection, and showback or chargeback should all rely on the same adjusted cost model.

- Consistency reduces confusion and improves trust in the numbers.

Creating Goodwill and Auditability with Accounting

- Strong account structure and tagging do more than support accountability.

- They also make spend easier to audit and easier for finance teams to trust.

- Richer and cleaner data leads to better forecasting and better cross-functional cooperation.

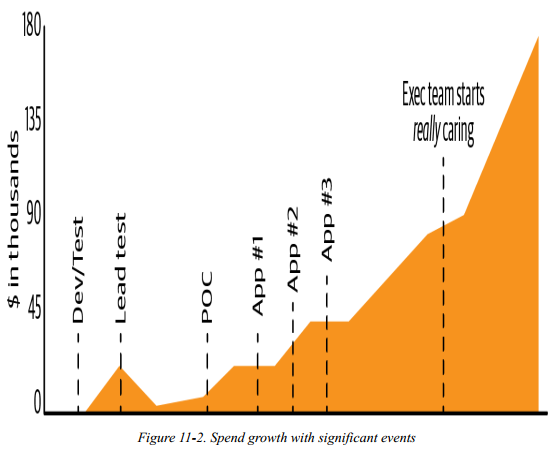

The Spend Panic Tipping Point

- Many organizations ignore cloud cost management until spend becomes large enough to attract executive attention. This is where RSM is at today.

- That tipping point often creates a sudden rush to explain and optimize cloud spend. This is what I do.

- Without a solid allocation model already in place, those conversations become difficult and avoidably tense.

Why Preparation Matters

- Spend panic is common and usually predictable.

- If teams already have defensible allocation and reporting, executive scrutiny becomes manageable.

- If they do not, organizations are forced into reactive cost conversations without enough evidence.

Note: An increasing bill is not bad if our business is growing. It becomes a problem when we have no way to explain why the bill is increasing.

Spreading out Shared Costs

- Shared IT and platform costs are common in cloud environments.

- These can include support charges, shared Kubernetes clusters, data platforms, networking, logging, or monitoring systems.

- A mature allocation strategy does not leave these costs trapped in a central bucket without explanation.

- Proper tagging and spliiting shared costs across consumers creates a more accurate picture of who is really consuming what.

Common Shared Cost Allocation Models

- Proportional: distribute shared cost based on each team’s share of direct spend.

- Even split: divide the total equally across targets.

- Fixed: distribute cost using a user-defined allocation ratio. Needs to total 100%

Why Proportional Allocation Is Common

- Proportional allocation is often the most defensible because it ties shared cost to relative usage or spend.

- It makes team totals more realistic than leaving shared costs fully centralized.

- This gives teams a truer understanding of the cost of the services they consume.

Chargeback Versus Showback

Showback leaves a bill on the table for analysis; chargeback leaves the same bill, but requires payment. - Barry Whittle from Apptio :)

- Showback means teams see what they spent, but the cost is still funded centrally.

- Chargeback means those costs are pushed directly onto the responsible team’s budget or P&L.

- Both drive accountability, but chargeback carries stronger financial consequences.

Note: Angry accountants do not make good FinOps partners. Showback is often a more practical starting point for organizations new to FinOps, while chargeback is a more direct accountability model that may require more maturity in financial processes and data quality.

A Combination of Models Fit for Purpose

When Showback Makes Sense

- Showback works well when an organization wants accountability without immediately changing internal accounting behavior.

- It is often the easier model to adopt first.

- Teams gain visibility, learn to forecast, and build trust in the data before costs hit their books directly.

When Chargeback Makes Sense

- Chargeback is useful when accounting, tax, or organizational structure requires costs to be allocated directly to business owners.

- It is typically more mature operationally because it needs stronger data quality and financial process alignment.

- Not every organization needs or wants to go all the way to chargeback.

Chargeback Can Take Time

- Organizations often move from exploratory cloud use, to showback, and only later to full chargeback.

- This transition may take years because finance, budgeting, and team-level ownership all need to mature together.

- Showback often serves as the training ground for eventual chargeback.

A Mixed Model Can Be Practical

- Some organizations use showback for certain workloads and chargeback for others.

- The right choice depends on financial structure, workload type, and the reporting needs of the business.

- Fit-for-purpose models are often more realistic than enforcing one method everywhere.

Note: It’s a common challenge that many FinOps teams encounter. The way engineers tag resources doesn’t necessarily align to the way the business needs to report cloud spend. And spending often needs to be remapped to match the cost centers or products that are the rightful owners of cloud spend.

Account Structure and Tagging Are Foundational

- Allocation strategy depends on good cloud account organization.

- Account hierarchies, account naming, and tagging are the first layers of cost attribution.

- These structures create the base from which more advanced allocation logic can operate.

Strategy:

- Account hierarchy: organize accounts to reflect ownership, environment, or application boundaries.

- Account naming: use consistent naming conventions that capture business context.

- Tagging: apply tags that identify cost centers, products, teams, and other relevant metadata for allocation.

- Shared costs across accounts: use tagging and allocation rules to distribute shared costs fairly across consumers.

Key Building Blocks of Allocation

- Account hierarchies that isolate environments, teams, or applications.

- Naming standards that capture meaningful business context.

- Tagging strategies that separate costs inside shared accounts.

- Methods for spreading shared costs and adjusting spend to match reality.

Tagging Will Never Be Perfect

- Not all resources are taggable.

- Not all teams are perfectly compliant with tagging standards.

- Mature FinOps teams therefore track untagged spend as a data hygiene metric and continue improving it over time.

Fully Adjusted Costs Improve Decisions

- Over time, strong FinOps practices move toward showing teams fully adjusted costs.

- These include amortization, shared cost distribution, and accurate discount treatment.

- That gives teams a more honest view of what their cloud usage really costs.

Note:

- Following a typical FinOps maturity curve, Ally initially kept cloud volume discounts, enterprise support charges, and prepayments such as RI amortization out of the reporting shown to end teams.

- Over time, her FinOps practice matured, and those costs were increasingly factored into team spend reporting.

- Today, her teams see properly adjusted prices with amortization and accurate volume rates built into the numbers.

- That gives them a more accurate picture of actual cost.

Showback Model in Action

- Effective showback ties actual spending to the right team and compares it to forecast and budget.

- It should be available at multiple cadences, including weekly, monthly, and quarterly views.

- Good showback also highlights cost drivers and emerging anomalies before monthly reviews become difficult.

Operating Reviews and Variance Management

- Leadership reviews should surface major spend variances early.

- When variance is caught quickly, teams can investigate root causes and respond before the monthly close process.

- This is a good example of how FinOps improves collaboration and speeds decision-making.

Chargeback and Showback Considerations

- Organizations can pass through actual costs directly.

- A central team may keep part of commitment or negotiated discount savings.

- Some organizations use these retained savings to fund central administration.

- The tradeoff is that less transparent models may conflict with mature FinOps ideals.

Strategy:

- Charge back actual costs directly to teams for maximum accountability and transparency.

- Centralize commitment-based discounts and keep some portion of those savings to fund FinOps administration and optimization efforts.

- Centralize negotiated discounts

Executive and Finance Alignment Is Required

- Allocation model decisions affect internal budgeting, accounting, and P&L behavior.

- Because of that, finance and accounting must be part of the design conversation.

- The ultimate choice is usually an executive decision, not just a tooling or reporting decision.

Strategic Lessons

- Allocation is one of the most important building blocks in FinOps.

- It should include adjusted rates, amortization, and shared costs wherever practical.

- Strong allocation improves auditability, trust, and accountability.

- Showback and chargeback are both valid, but they serve different organizational needs.

- It is better to have a scalable allocation model before a spend panic than to build one under pressure.

Conclusion

Allocation strategy varies from company to company, but it is a core building block in the FinOps lifecycle. It helps organizations focus on the right questions and clearly explain what they are spending on cloud and who is responsible for that spend.

- Cloud spend in a FinOps practice is typically viewed on an accrual basis, with amortized prepayments, discounted rates, and shared costs reflected in the data teams see.

- Shared costs such as support, amortization, and unallocated expenses should be factored into the allocation model wherever practical.

- Showback and chargeback both drive accountability.

- A showback or chargeback model can also improve tagging discipline and auditability.

- Chargeback is the more advanced model, but it is not the right fit for every organization because of accounting and operating constraints.

- A practical path is often to start with showback and then evaluate whether the organization is ready to move toward chargeback.

- Having a model in place before reaching a spend-panic tipping point makes it much easier to answer executive questions about what is driving spend.

Glossary

| Term | Definition |

|---|---|

| Accrual basis | A reporting basis where costs are recorded in the period when the benefit is realized, not simply when the invoice is paid. |

| Allocation construct | The set of rules, mappings, and structures used to assign cloud spend to the right teams, products, or business units. |

| Amortization | The process of spreading an upfront commitment or prepaid cost over the period in which its value is consumed. |

| Auditability | The ability to trace, verify, and explain cloud spending clearly enough for financial review and control. |

| Cash basis | A reporting basis where costs are recorded when payment occurs rather than when value is realized. |

| Chargeback | A model where cloud costs are allocated directly to the budget or P&L of the responsible team or business unit. |

| Fixed allocation | A shared-cost model where expenses are distributed according to a predefined percentage or coefficient. |

| Fully adjusted cost | Cloud cost data that includes amortization, shared costs, negotiated discounts, and other adjustments needed to reflect real effective spend. |

| Proportional allocation | A shared-cost model where expenses are distributed based on each target’s relative share of direct spend or usage. |

| Showback | A reporting model where teams are shown their actual cloud costs without necessarily charging those costs to their own budget or P&L. |

| Shared costs | Cloud or platform costs used by multiple teams that must be split fairly across consumers. |

| Spend panic | The point where cloud spend becomes large enough to trigger urgent executive scrutiny and reactive cost management. |

| Tagging strategy | The structured approach for applying metadata to resources so costs can be attributed, analyzed, and governed effectively. |

| Untagged spend | Cloud spending that cannot be mapped cleanly because required resource metadata is missing or incomplete. |

| Unit economics | Cost measures tied to business outcomes, such as cost per product, customer, or transaction. |